More than one-third of smart home device owners also own a voice-activated speaker, according to The NPD Group

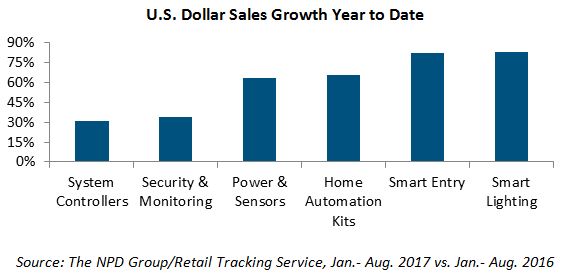

Port Washington, NY, October 5, 2017 – Fifteen percent of U.S. internet households currently own a home automation device, up from 10 percent in April 2016, according to global information provider, The NPD Group. Year to date, U.S. dollar sales of home automation products have increased 43 percent, with strong growth across all device types1. While security and monitoring continues to hold the largest share of dollar sales in the category, video doorbells2 (+123 percent) and smart lighting (+83 percent) are also quickly growing.

“The growth we are seeing in the number of owner homes is an indication that a broader field of available products, wider distribution, and greater awareness are actually adding users,” noted Ben Arnold executive director, industry analyst for The NPD Group. “Voice-enabled speakers have also played a key role in catalyzing interest in the smart home.”

According to the new Digital Voice Assistants: Ownership & Applications Report from NPD’s Connected Intelligence, ownership of voice-activated wireless speakers has more than tripled in a year's time, now totaling 10 percent of U.S. internet households. Of Amazon Echo and Google Home owners, 48 percent and 57 percent, respectively, reported buying their first home automation product after owning a voice-enabled speaker. In fact, 36 percent of existing smart home device owners also own a voice-activated speaker, and 65 percent of smart home device owners are interested in using voice commands to control other devices in their home.

As is often the case in emerging markets, younger consumers, aged 18-34, are the most likely to own a voice-activated wireless speaker, as well as a home automation device; but noticeable growth is also occurring in other age groups. Eleven percent of consumers aged 35-54 report owning a voice-enabled speaker, up from seven percent the prior year, while consumers 55+ grew to six percent from one percent. Similarly, 16 percent of consumers aged 35-54 report owning a home automation device, up from 11 percent the prior year, while consumers 55+ grew to eight percent from seven percent.

“The voice-enabled speaker market is expanding quickly, with a number of high-profile products expected to hit shelves in Q4 2017, and into 2018. As sales of these devices continue to grow, and more voice-enabled applications are developed, the use case for intelligent voice speakers, particularly as it relates to home automation devices, will continue to expand,” said Arnold.

1Source: The NPD Group/Retail Tracking Service, Home Automation, Jan.- Aug. 2017

2Source: The NPD Group/Retail Tracking Service, Smart Entry, Video Doorbells, Jan.- Aug. 2017

Methodology

The results of the NPD Group Connected Intelligence Digital Voice Assistants: Ownership & Applications Report draws data from the semi-annual Connected Home Automation Survey. The survey is based on consumer panel research that reached over 5,600 U.S. consumers, aged 18+ from diverse regions and demographical backgrounds. The resulting base was over 2,600 consumers that have used voice commands to operate a consumer electronics device. They reported on their experience with digital voice assistants, ownership of voice-activated speakers, and what will drive or impede their adoption. This survey was fielded from April 7-21, 2017. Trended results are compared to a study fielded from April 11-25, 2016.

Press Contact

Megan Scott

516-625-7516

megan.scott@npd.com

The NPD Group, Inc.

900 West Shore Road

Port Washington, NY 11050